7 March 2024

The 2024 Budget was considered by many to be quite restrained – with the main headline being around the cut in National Insurance (“NI”) from 10% to 8%. This, combined with the previous 2% cut, will save the average employee over £900 per year.

Here are some of the key changes that may affect your business and employees:

Change to National Insurance rates

This headline measure will be introduced in April 2024 -a reduction from 10% to 8% which will result in many employees receiving an increase in take home pay – a welcome boost to offset the ongoing cost of living crisis.

The employer NI rate remains at 13.8%, but employers should make provision to ensure their payroll processes capture the NIC reduction.

Child benefit changes

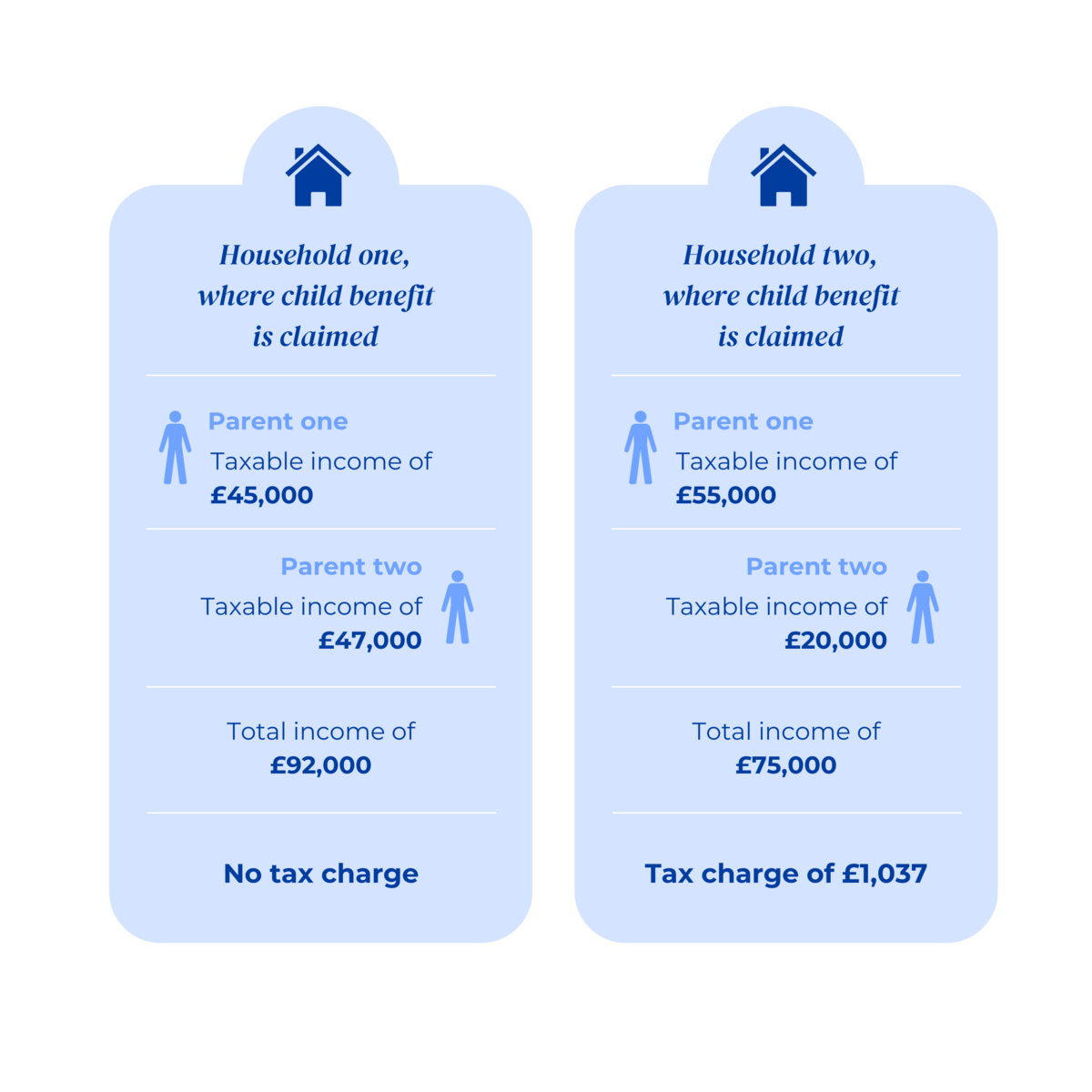

Child benefit support is available to parents with earnings below a certain level (£50,000 in the 2023/24 tax year). In order to manage this, a tax charge applies should a claim be made and earnings of one or both parents exceed £50,000. The aim of this tax charge is to ensure that this child benefit is targeted to those families who have the greatest need for support.

There is still an ongoing issue with how the “higher income child benefit charge” (the starting threshold being where one parent’s taxable income hits £50,000) interacts with the tax system. This is because one aspect (tax) is based on an individual, and the other (child benefit) is based on a household. This has resulted in situations which could be considered to be unfair.

Although the government plan is to change this methodology, it will not be actioned until April 2026 due to complexity. In the meantime, the threshold at which the higher income child benefit charge starts to apply will shift from £50,000 to £60,000 effective from 6th April 2024.

There are mitigation strategies that employees can apply to reduce their tax burden, and even move to an eligible earnings threshold – such as salary sacrifice for pension contributions or other benefits such as EVs.

Effective tax rate of over 60% - an opportunity missed?

This remains an ongoing issue for higher earners. Currently, once an individuals’ taxable pay goes above £100,000 per annum, they start to see their personal allowance (the part of our pay that we do not pay tax on - £12,570 in the 2023/24 tax year) erode. This gives an effective tax rate of 60% (i.e., their higher rate tax of 40% plus 20% where that personal allowance is removed), plus National Insurance of 2%.

Any employee impacted by this should consider using salary exchange to manage their taxable income to avoid that very high effective level of tax, and if they have a young family, reducing earnings below the £100k threshold could make them eligible for free childcare provision.

Pension Pot for life?

The Government’s previous announcement on considering whether employers should pay into a pension policy of the employee’s choice was again highlighted, but with no further update on timeline.

Our concern continues to be the additional burden for businesses - additional administration, payroll complexity, governance, and engagement. And for employees – concerns around higher management charges, lack of governance and investment advice and options at retirement remain.

If you would like to discuss any of the points in this article in more detail, please contact Rob Marshall.

Rob Marshall

Sales Director – Employee Benefits

T: +44 (0) 7704 547478

E: rob.marshall@verlingue.com